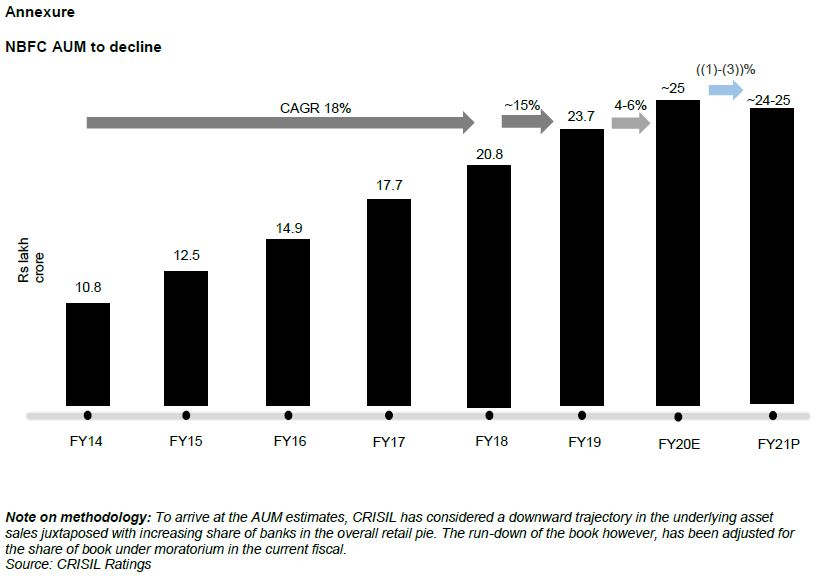

Assets under management (AUM) of non-banking financial companies1 (NBFCs) are expected to de-grow 1-3% (see chart in annexure) in the current fiscal as fresh disbursements drop sharply. Excluding the top 5 NBFCs, the de-growth is expected to be even sharper at 7-9%. Lower repayments during the loan moratorium period (March 1, 2020, to August 31), and capitalisation of interest accumulated will, however, help limit the de-growth.

As for disbursements, four factors at play: one, the challenging macroeconomic environment, which would curb underlying asset sales, especially in the two biggest segments of housing and vehicle finance; two, sharper focus on liquidity as incremental funding is not easy to come by for many players in a confidence-sensitive scenario; three, stiff competition from banks as funding costs for many NBFCs remain relatively high; and, four, tightening of underwriting standards by NBFCs amid weak economic activity and expectations of increasing delinquencies.

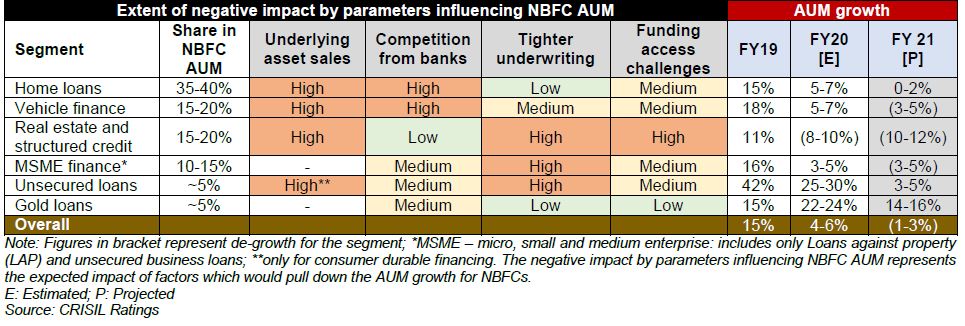

Says Krishnan Sitaraman, Senior Director, Crisil Ratings, “While disbursements across segments are expected to fall 50-60%, AUM trajectory will differ by segment. Crisil’s analysis of the largest segments of the NBFC AUM pie shows that most segments could witness contraction in the current fiscal. The silver lining, however, would be gold loans, which constitute ~5% of the AUM. Growth here is seen to be relatively higher as more individuals and micro enterprises go for it to meet immediate funding needs.”

For majority of the NBFCs, multiple factors will be at play this fiscal, as the table below shows:

Mumbai

Mumbai